Creating a new mechanism¶

[1]:

import numpy as np

import pandas as pd

import pymarket as pm

import matplotlib.pyplot as plt

from pprint import pprint

One of the advantages of PyMarket is the ability to easily implement and test a new idea for a mechanism. Here we will show how to implement a new mechanism and use it.

The uniform price mechanism¶

We are going to implement a uniform price mechanism that charges every trading player the clearing price.

As a reference we are going to be implement the example Here

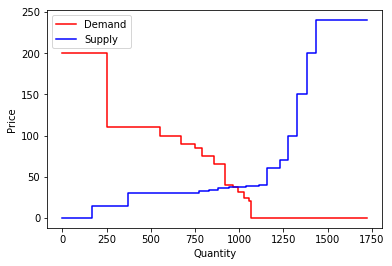

We can begin by adding the corresponding bids to a new market

[2]:

mar = pm.Market()

buyers_names = ['CleanRetail', 'El4You', 'EVcharge', 'QualiWatt', 'IntelliWatt']

mar.accept_bid(250, 200, 0, True) # CleanRetail 0

mar.accept_bid(300, 110, 1, True) # El4You 1

mar.accept_bid(120, 100, 2, True) # EVcharge 2

mar.accept_bid( 80, 90, 3, True) # QualiWatt 3

mar.accept_bid( 40, 85, 4, True) # IntelliWatt 4

mar.accept_bid( 70, 75, 1, True) # El4You 5

mar.accept_bid( 60, 65, 0, True) # CleanRetail 6

mar.accept_bid( 45, 40, 4, True) # IntelliWatt 7

mar.accept_bid( 30, 38, 3, True) # QualiWatt 8

mar.accept_bid( 35, 31, 4, True) # IntelliWatt 9

mar.accept_bid( 25, 24, 0, True) # CleanRetail 10

mar.accept_bid( 10, 21, 1, True) # El4You 11

sellers_names = ['RT', 'WeTrustInWind', 'BlueHydro', 'KøbenhavnCHP', 'DirtyPower', 'SafePeak']

mar.accept_bid(120, 0, 5, False) # RT 12

mar.accept_bid(50, 0, 6, False) # WeTrustInWind 13

mar.accept_bid(200, 15, 7, False) # BlueHydro 14

mar.accept_bid(400, 30, 5, False) # RT 15

mar.accept_bid(60, 32.5, 8, False) # KøbenhavnCHP 16

mar.accept_bid(50, 34, 8, False) # KøbenhavnCHP 17

mar.accept_bid(60, 36, 8, False) # KøbenhavnCHP 18

mar.accept_bid(100,37.5, 9, False) # DirtyPower 19

mar.accept_bid(70, 39, 9, False) # DirtyPower 20

mar.accept_bid(50, 40, 9, False) # DirtyPower 21

mar.accept_bid(70, 60, 5, False) # RT 22

mar.accept_bid(45, 70, 5, False) # RT 23

mar.accept_bid(50, 100, 10, False) # SafePeak 24

mar.accept_bid(60, 150, 10, False) # SafePeak 25

mar.accept_bid(50, 200, 10, False) # SafePeak 26

[2]:

26

[3]:

12, 15, 22, 23

[3]:

(12, 15, 22, 23)

[4]:

mar.plot()

Implementing the mechanism¶

All market mechanisms take as arguements a bids dataframe (as well as possibly extra parameters) and returns a TransactionManager and an extras dictionary.

[13]:

def uniform_price_mechanism(bids: pd.DataFrame) -> (pm.TransactionManager, dict):

trans = pm.TransactionManager()

buy, _ = pm.bids.demand_curve_from_bids(bids) # Creates demand curve from bids

sell, _ = pm.bids.supply_curve_from_bids(bids) # Creates supply curve from bids

# q_ is the quantity at which supply and demand meet

# price is the price at which that happens

# b_ is the index of the buyer in that position

# s_ is the index of the seller in that position

q_, b_, s_, price = pm.bids.intersect_stepwise(buy, sell)

buying_bids = bids.loc[bids['buying']].sort_values('price', ascending=False)

selling_bids = bids.loc[~bids['buying']].sort_values('price', ascending=True)

## Filter only the trading bids.

buying_bids = buying_bids.iloc[: b_ + 1, :]

selling_bids = selling_bids.iloc[: s_ + 1, :]

# Find the long side of the market

buying_quantity = buying_bids.quantity.sum()

selling_quantity = selling_bids.quantity.sum()

if buying_quantity > selling_quantity:

long_side = buying_bids

short_side = selling_bids

else:

long_side = selling_bids

short_side = buying_bids

traded_quantity = short_side.quantity.sum()

## All the short side will trade at `price`

## The -1 is there because there is no clear 1 to 1 trade.

for i, x in short_side.iterrows():

t = (i, x.quantity, price, -1, False)

trans.add_transaction(*t)

## The long side has to trade only up to the short side

quantity_added = 0

for i, x in long_side.iterrows():

if x.quantity + quantity_added <= traded_quantity:

x_quantity = x.quantity

else:

x_quantity = traded_quantity - quantity_added

t = (i, x_quantity, price, -1, False)

trans.add_transaction(*t)

quantity_added += x.quantity

extra = {

'clearing quantity': q_,

'clearing price': price

}

return trans, extra

Wrapping the algorithm as a mechanism¶

[14]:

# Observe that we add as the second argument of init the algorithm just coded

class UniformPrice(pm.Mechanism):

"""

Interface for our new uniform price mechanism.

Parameters

-----------

bids

Collection of bids to run the mechanism

with.

"""

def __init__(self, bids, *args, **kwargs):

"""TODO: to be defined1. """

pm.Mechanism.__init__(self, uniform_price_mechanism, bids, *args, **kwargs)

Adding the new mechanism to the list of available mechanism of the market¶

[15]:

pm.market.MECHANISM['uniform'] = UniformPrice

Running the new mechanism and comparing it with Huang’s and P2P¶

[24]:

stats = {}

for mec in ['uniform', 'huang', 'p2p']:

t, e = mar.run(mec)

stat = mar.statistics()

stats[mec] = stat

Profits for the players in the different mechanism¶

[33]:

profits = pd.DataFrame([v['profits']['player_bid'] for k, v in stats.items()]).T

profits.columns = stats.keys()

profits

[33]:

| uniform | huang | p2p | |

|---|---|---|---|

| 0 | 42275.0 | 41529.375 | 22890.0 |

| 1 | 24375.0 | 23849.375 | 12980.0 |

| 2 | 7500.0 | 7246.250 | 3150.0 |

| 3 | 4215.0 | 3997.500 | 2630.0 |

| 4 | 2012.5 | 1816.875 | 1162.5 |

| 5 | 7500.0 | 7500.000 | 14647.5 |

| 6 | 1875.0 | 1875.000 | 810.0 |

| 7 | 4500.0 | 4500.000 | 18500.0 |

| 8 | 565.0 | 565.000 | 3910.0 |

| 9 | 0.0 | 0.000 | 4570.0 |

| 10 | 0.0 | 0.000 | 375.0 |

Percentage traded by mechanism¶

[36]:

traded = pd.DataFrame([v['percentage_traded'].round(3) for k, v in stats.items()]).T

traded.columns = stats.keys()

traded

[36]:

| uniform | huang | p2p | |

|---|---|---|---|

| 0 | 0.934 | 0.883 | 0.995 |

Percentage of the maximum social welfare achieved by mechanism¶

[38]:

welfare = pd.DataFrame([v['percentage_welfare'].round(3) for k, v in stats.items()]).T

welfare.columns = stats.keys()

welfare

[38]:

| uniform | huang | p2p | |

|---|---|---|---|

| 0 | 1.0 | 0.98 | 0.903 |

[ ]: